The market no longer believes in a ceasefire headline on its own. Africa is no longer dealing only with the first-round panic from the US-Iran war. It is now facing a more dangerous phase: a fragile truce, disrupted shipping, volatile energy prices, and second-round pressure on food, currencies, debt, and growth.

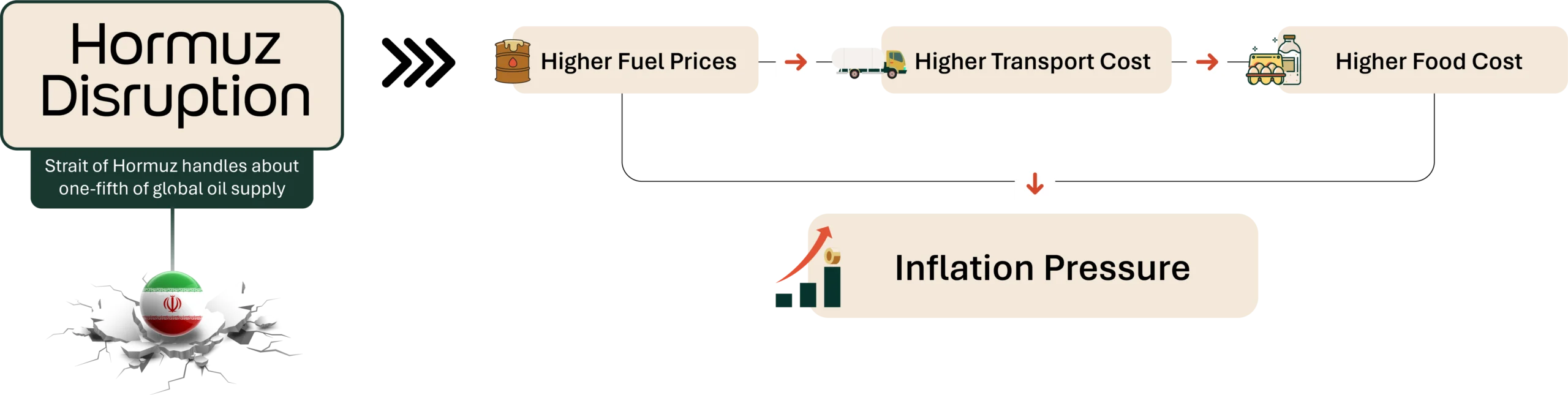

That shift matters because the current situation is more complex than the initial blockade shock. On April 17, 2026, Iran temporarily reopened the Strait of Hormuz following a ceasefire agreement. Still, by April 18, 2026, it had warned mariners that the strait was closed again and reimposed strict control through forces linked to the Islamic Revolutionary Guard Corps. On Sunday, April 19, the US military said it fired on an Iranian-flagged cargo ship as the vessel sailed toward Iran’s Bandar Abbas port, while President Donald Trump later said the United States had taken custody of the ship. Iran vowed retaliation, and shipping through Hormuz fell back close to a standstill. By April 20, Reuters reported only three crossings in 12 hours, versus a normal flow of about 130 vessels a day.

At the same time, markets are trying to price two conflicting realities. One is escalation: according to Reuters, Brent crude futures settled $5.10, or 5.64%, higher at $95.48 a barrel on Monday, April 20, 2026, as uncertainty over US-Iran peace talks and renewed violence around the Strait of Hormuz pushed oil prices higher. The other is diplomacy: by early April 21, Brent had eased to about $94.53 as investors bet peace talks in Pakistan could extend the ceasefire or produce a broader agreement.

Why the US-Iran war impact on Africa has changed

The current problem is not just the existence of a blockade. It is that Africa is absorbing the second-round effects of a war that has moved from battlefield shock to economic persistence. The IMF now projects global growth of 3.1% in 2026 and 3.2% in 2027, warning that the slowdown and inflation pickup will be especially pronounced in emerging markets and developing economies.

Sub-Saharan Africa is already feeling that pressure. The World Bank says Sub-Saharan African growth is holding at 4.1% in 2026, but downside risks are mounting as fuel, food, and fertilizer costs rise and financial conditions tighten. It also says Sub-Saharan African inflation is projected to reach 4.8% in 2026, while external public debt service-to-revenue has doubled from 9% in 2017 to 18% in 2025.

In plain terms, Africa is being hit at a moment when many governments have less room than they need to absorb another imported shock.

That is why the US-Iran war's impact on Africa is no longer only about commodity prices. It is about pass-throughs. How much of this disruption reaches pump prices, fertilizer orders, transport costs, exchange rates, sovereign financing, and household purchasing power? That is now the more important African macro question.

1. Africa fuel inflation is now the first policy stress point

The first effects of the renewed hostilities will be felt at the pump stations as fuel prices soar. Hormuz still handles one-fifth of global oil supply, and traffic through the strait remains limited even as talks flicker on and off. Citigroup told Reuters that another month of disruption could push prices toward $110 a barrel in the second quarter, while Societe Generale said higher prices have already cut oil demand by about 3%.

For Africa, the issue is not just the oil price itself. It is a domestic transmission. Nigeria shows the paradox most clearly. Reuters reported that petrol prices there have risen by more than 50% and diesel by more than 70% since the conflict began, even though higher crude prices have boosted export earnings. Bonny Light has climbed above $120 a barrel, but the same shock is also raising living costs and threatening to derail reforms.

South Africa captures the other side of the map. As a net fuel importer, it is more directly exposed to higher oil prices and weaker risk appetite. Reuters reported on April 20 that the rand and government bonds came under pressure again as renewed Hormuz disruption pushed oil prices higher.

What this means for policymakers

The policy trap is familiar. Higher fuel costs raise transport and production costs, feed into inflation, and force central banks and finance ministries into harder trade-offs. Countries that have already removed subsidies or tightened budgets now have less political room to cushion households. Countries that reintroduce broad support risk damaging fiscal credibility just as financing conditions worsen.

2. Africa's food security is becoming the bigger second-round risk

The second effect is food and fertilizer. This is where the story becomes more dangerous than a conventional oil shock. Reuters reported that the G20 is now holding additional talks on the war’s impact on food and fertilizer, with IMF-linked discussions warning that supply disruptions, especially at the start of the growing season, could leave 45 million more people facing food insecurity.

The African-specific risk is already visible. A joint AU–AfDB–UN report warned that if the conflict lasts more than six months, African economies could lose 0.2 percentage points of GDP growth in 2026, and that some African countries could be hit harder by fertilizer shortages than by higher oil prices. The same report noted that the Middle East accounts for 15.8% of Africa’s imports and 10.9% of its exports, underscoring that the transmission channel is structural, not incidental.

This matters because fertilizer shortages not only raise farm costs. They can lower application rates, reduce yields, distort planting decisions, and keep food inflation elevated long after the initial shipping shock. In lower-income African economies, where food takes up a large share of household spending, that makes fertilizer is a macroeconomic variable, not just an agricultural one.

Why is this a bigger African problem than a global one?

Advanced economies feel energy spikes mainly through disposable income. Africa often feels them through both income and food systems at once. That makes second-round effects more socially and politically destabilizing. It also explains why food resilience, logistics, storage, and fertilizer access are now part of macro policy, not just sector policy. This is an inference from the World Bank’s inflation warning and the G20’s fertilizer focus.

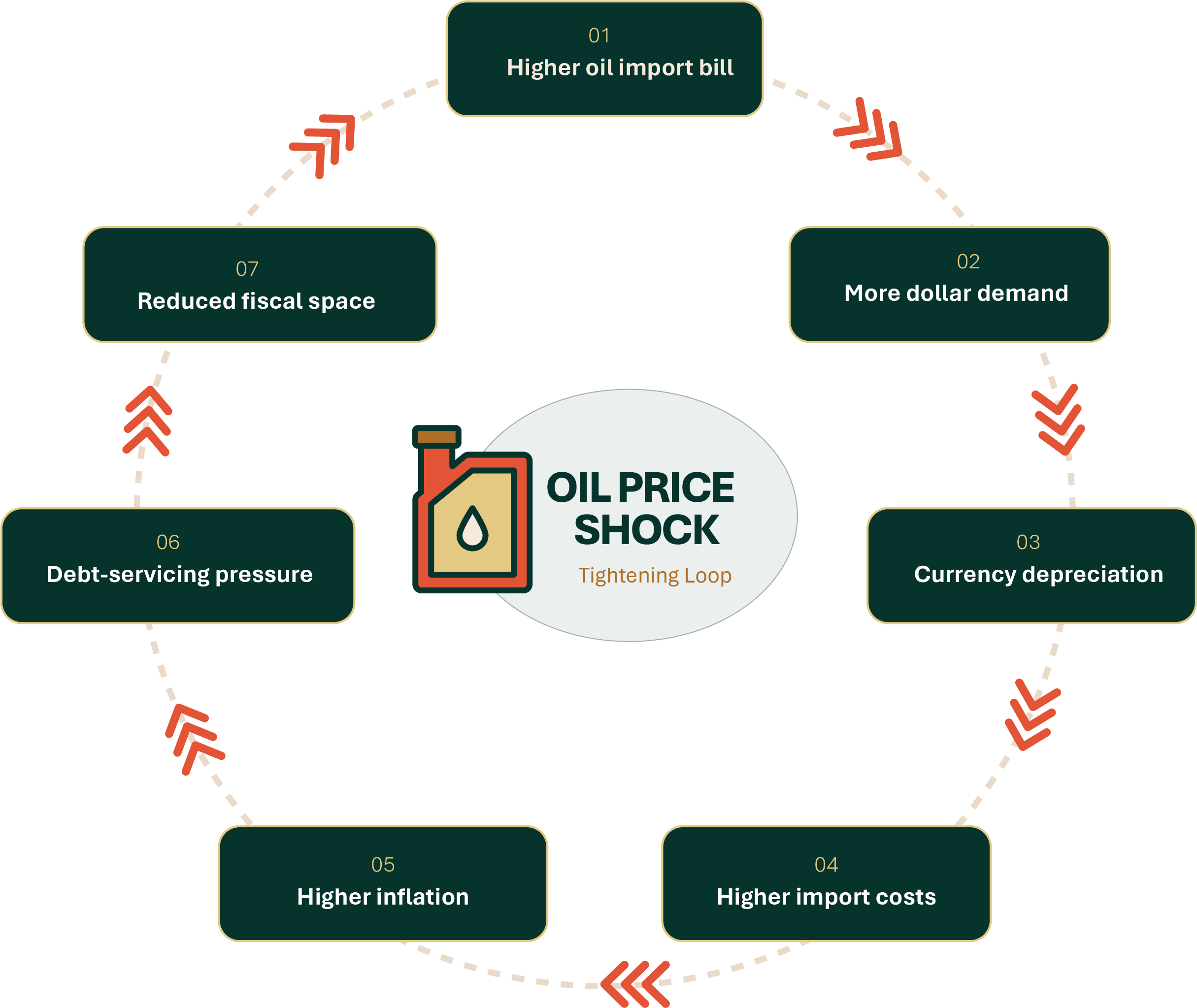

3. Africa's debt stress and FX pressure are tightening policy space

The third effect is financial. Higher oil prices worsen current accounts for fuel importers, weaken currencies, and make imports more expensive in local terms. That raises inflation further and leaves central banks with fewer easy choices. At the same time, debt service burdens are already high. The World Bank’s latest Africa update says external public debt service-to-revenue has reached 18%, up from 9% in 2017.

There are already concrete examples. Kenya has requested emergency World Bank support to cushion the shock. Reuters reported that Nairobi is seeking rapid financing, has cut VAT on petroleum temporarily, lowered its 2026 growth forecast to 5.3% from 5.5%, and is leaning on reserves above $13 billion to keep the volatility of the Kenyan Shilling orderly.

The broader pattern is continental. AfDB said this month that 29 African currencies have weakened since the conflict began, raising the cost of importing fuel, food, and fertilizer and making external debt servicing more expensive. Reuters also reported that at least 12 countries are now expected to seek IMF programs because of the crisis.

The investor implication

This is where the map of risk starts to matter more than the headline oil price. Countries with stronger reserves, more credible monetary policy, and better fiscal signaling will absorb the shock more smoothly. Countries with weaker buffers, large fuel-import dependence or acute refinancing needs are more exposed to abrupt pressure on FX, bonds, and domestic prices.

4. The US-Iran war impact is splitting the continent unevenly

The fourth effect is divergence. The winners and losers do not line up neatly between oil exporters and oil importers. Nigeria and Angola can benefit from stronger crude revenues, but that does not automatically shield households from inflation or protect reform programs. Angola, for example, expects higher oil revenue to cushion some of the fallout, while Nigeria is already showing how crude upside can coexist with a domestic fuel squeeze.

Meanwhile, oil-importing economies face a more direct squeeze through fuel bills, trade balances, and currencies. The World Bank has said countries such as Burundi, Malawi, Ethiopia, Kenya, and Mozambique are among the most exposed. Reuters’ reporting on Kenya’s emergency support request reinforces that view.

There is a third category too: limited logistics beneficiaries. The AU–AfDB–UN report says rerouted transport is increasing traffic through ports such as Maputo, Durban, Walvis Bay, and Mauritius. But that upside is narrow. It is not large enough to offset the broader continental drag from higher inflation, tighter financing, and disrupted supply chains.

Africa versus global markets

Globally, the economic story is still centered on oil, gas, and growth. In Africa, the same shock is more layered. It hits fuel costs, fertilizer flows, exchange rates, debt service, and household welfare at the same time. That makes the continent more vulnerable in the short term, but it also clarifies where resilience must come from: better energy security, more diversified food-input supply, deeper domestic capital buffers, and faster regional trade integration.

This is the Pan-African reading of the crisis. Africa is not simply an external victim of Middle East turbulence. The continent’s response will shape whether this becomes another imported inflation episode or a catalyst for more serious investment in domestic refining, fertilizer resilience, logistics, and industrial policy. The World Bank’s latest Africa update explicitly argues that better-designed industrial policy, embedded in infrastructure, skills, finance, and regional integration, is central to stronger long-run growth.

Bottom line

The original question fixates on the issue of whether Africa should treat this event as more than a distant Middle East security story. The answer is even clearer now: yes. But the reason has changed. The immediate oil shock has become a broader second-round macro shock. A fragile ceasefire has not restored normal shipping. Oil is volatile, not resolved. Food and fertilizer have moved to the center of the policy debate. And debt-stretched African governments are confronting the crisis with limited buffers.

For policymakers, the priorities are now clearer than diplomacy. Protect vulnerable households with targeted support, not broad subsidies. Preserve FX buffers. Secure fuel and fertilizer access. Save any commodity windfall rather than spending it too quickly.

A useful example is China’s Dibao, or minimum livelihood guarantee system. The programme provides targeted cash support to low-income households, especially in rural areas, rather than using broad price controls that benefit rich and poor households alike. For selected African economies, this type of targeted cash-transfer model could be useful if three conditions are in place: a reliable social registry, strong digital payment infrastructure, and transparent verification of beneficiaries.

It would not work as a simple copy-and-paste model everywhere. In countries with weak identity systems, fragmented rural records, or limited mobile-money penetration, cash transfers can suffer from leakages and exclusion errors. But where digital ID, mobile payments, and community-level beneficiary verification are improving, targeted transfers can help governments cushion poor households without reopening expensive fuel subsidies.

For investors and businesses, the signal is equally clear: this is no longer only a Middle East headline. It is a live test of Africa’s inflation resilience, external financing strength, and reform credibility.

Explore more LEAF analysis on Africa’s growth outlook, inflation risks, energy security, and sector opportunities as global shocks reshape the continent’s macro landscape.

External authority references

US-Iran Peace Deal: Africa’s Economic Test

The U.S.-Iran peace framework matters for Africa not because it resolves the continent’s structural vulnerabilities, but because it temporarily reprices several global risks to which African economies are…

Continue reading

Share a market signal, question, or useful perspective. You can respond to the article as a whole, or use the "Discuss this section" buttons beside key points to add context.

The discussion space is open. Add a clear observation, a question worth exploring, or a field signal that could help other readers think more sharply.