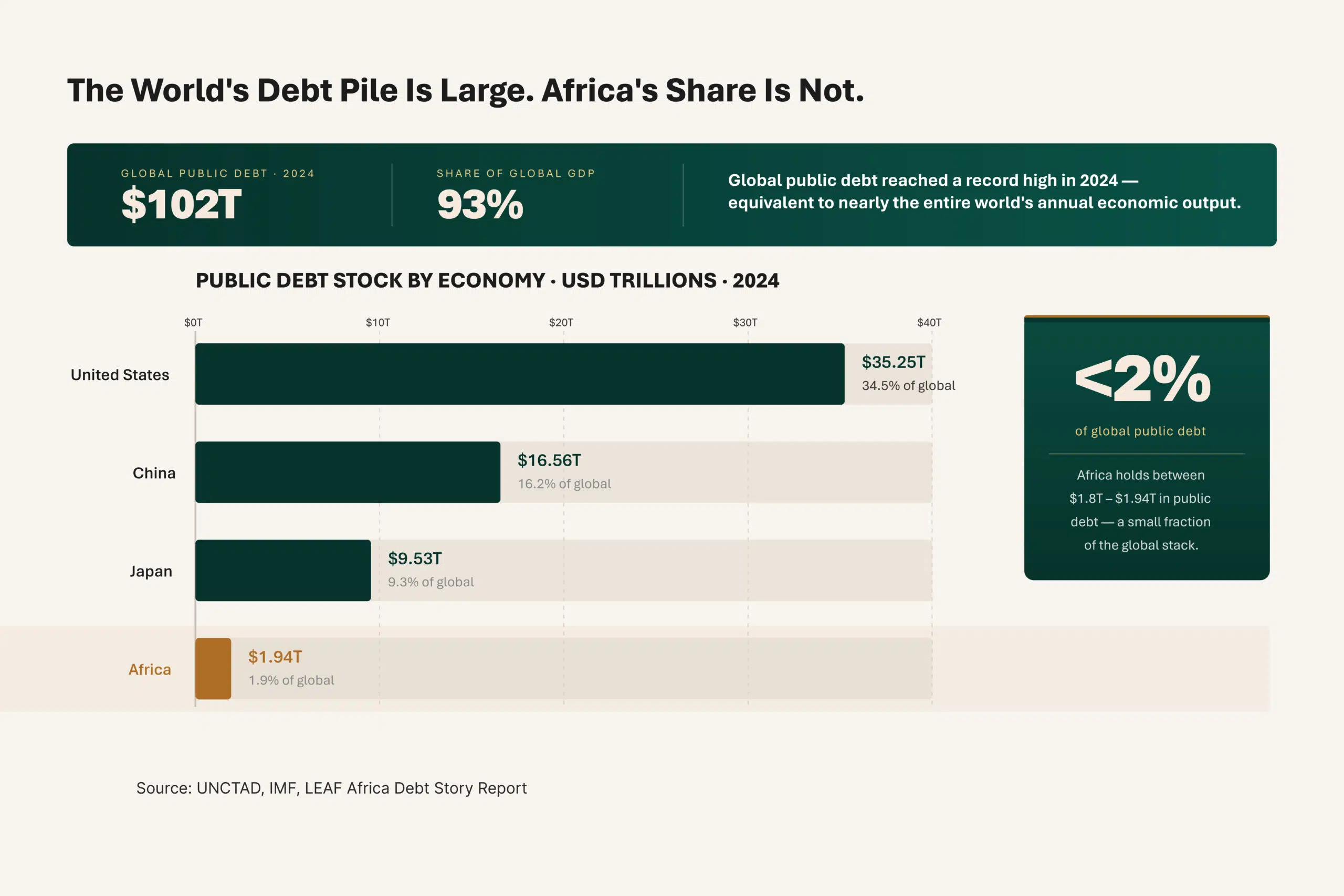

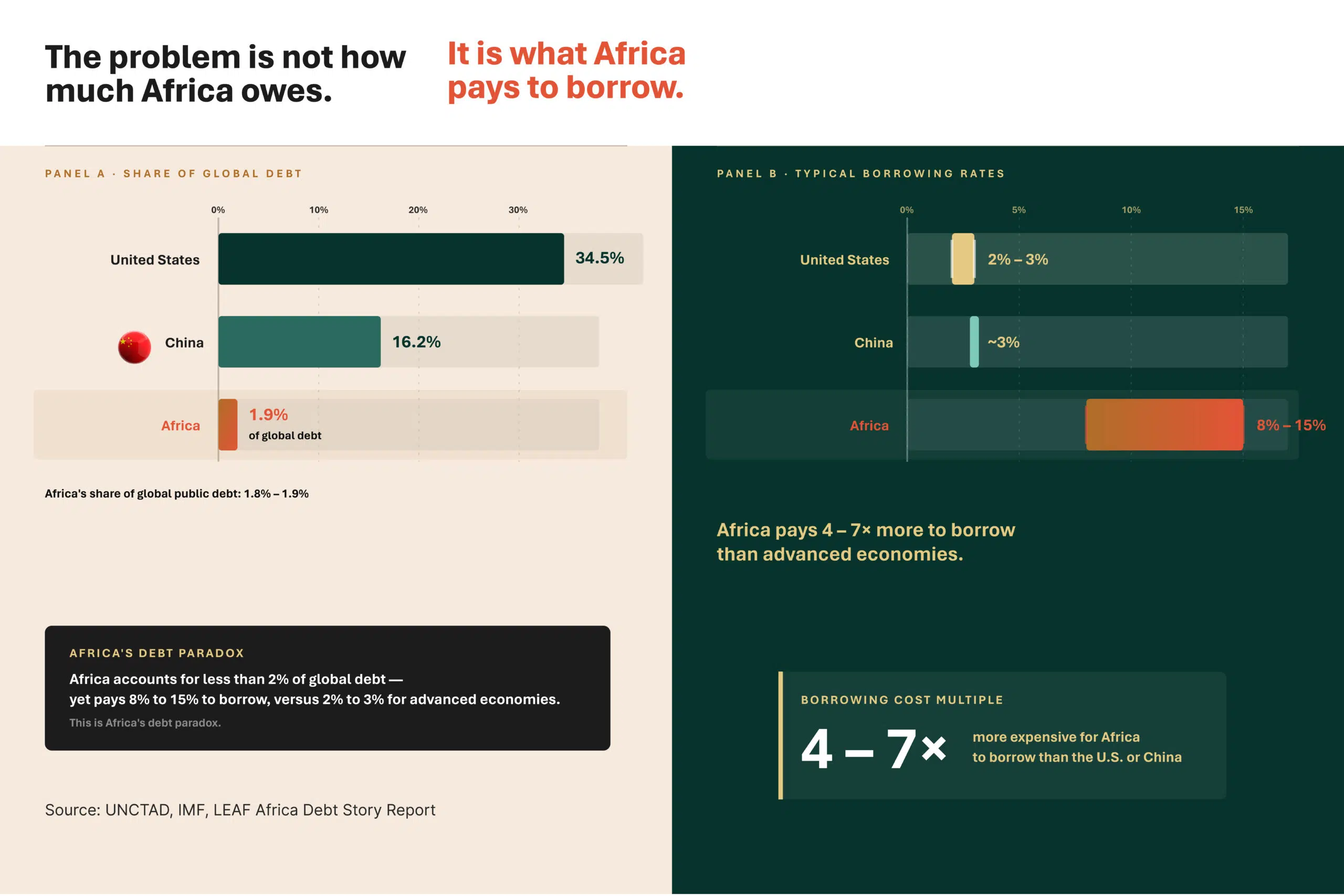

Global public debt reached a record $102 trillion in 2024, equal to 93% of global GDP. Africa accounts for only about 1.9% of that debt, yet many African economies borrow at rates of 8% to 15%, compared with roughly 2% to 3% for the United States and China.

That is the imbalance at the center of Africa’s debt story.

The issue is not simply how much countries owe. It is how much they pay to borrow, how fast global debt is rising, and why the same financial system gives cheaper money to countries that already hold the largest debt stocks.

The world is living in an era of record debt, but not every country experiences debt the same way. For Africa, the problem is not only scale. It is price.

Why Global Debt Matters Now

Public debt is no longer a developing country’s issue. It is a global economic condition.

According to LEAF Africa’s Debt report, global public debt stood at $102 trillion in 2024, rising by 5.15% from 2023 and reaching the equivalent of 93% of global GDP. The largest debt holders were the United States at $35.25 trillion, China at $16.56 trillion, and Japan at $9.53 trillion. Africa’s debt stood at about $1.94 trillion, representing just 1.9% of the global total.

The report also notes a sharp acceleration in global debt, from $102 trillion in 2024 to $251 trillion by September 2025, underscoring the speed and scale of the current build-up.

For investors, policymakers, and businesses, this matters because debt shapes interest rates, currency stability, fiscal space, infrastructure funding, and private-sector access to capital.

Debt is not just a line in a government balance sheet. It influences the price of money across the whole economy.

What Is Happening: The World Is Borrowing More

Governments borrow when revenues are not enough to meet spending needs.

Governments generate income from taxes, fees, exports, and state-owned enterprises. They spend money on salaries, roads, schools, hospitals, defense, and public services. When expenses exceed income, governments borrow rather than halt essential spending or long-term development projects.

This makes borrowing a normal part of public finance.

Debt can help governments:

- Fund budget gaps when tax revenues are insufficient

- Invest in long-term infrastructure such as roads, power, and healthcare systems

- Stabilize the economy during crises such as pandemics, wars, and recessions

The problem begins when borrowing becomes too expensive, too frequent, or poorly linked to productive investment.

Why the World Is Borrowing More

The current global debt build-up is driven by several overlapping pressures, such as ageing populations, war-induced inflation, geopolitical tensions, and COVID-19 relief measures, as major drivers of sovereign borrowing. Ageing populations increase pension, healthcare, and social protection spending. War-induced inflation raises borrowing costs and creates emergency fiscal pressures. Geopolitical tensions increase defense and resilience spending.

COVID-19 added a major shock; $9 trillion in global fiscal support by April 2020 and $17.2 trillion in announced public stimulus by July 2021.

This means the post-pandemic world is not only dealing with higher debt levels. It is also dealing with higher interest rates, weaker fiscal buffers, and more expensive refinancing.

The global pattern is clear

Advanced economies borrowed heavily to protect households, companies, and financial systems. Developing economies borrowed to fund emergency spending, stabilize currencies, and maintain basic public services.

But the cost of that borrowing was not equal.

This is where Africa’s debt story becomes different.

The Cost of Debt, Not Just the Size

Africa’s share of global debt is small. Its borrowing cost is not.

The LEAF Africa debt story report shows that the United States holds 34.5% of global public debt, China holds 16.2%, and Africa holds only 1.9%. Yet the United States and China borrow at roughly 2% to 3%, while many African countries borrow at 8% to 15%.

This creates a fundamental imbalance.

Large economies can carry huge debt stocks because they often borrow in their own currencies, have deeper capital markets, enjoy stronger investor confidence, and benefit from lower perceived default risk. African countries often borrow under tougher conditions because investors price in currency volatility, weaker fiscal positions, lower liquidity, political risk, and external vulnerability.

The result is a global debt system where countries with smaller debt shares may face heavier debt stress.

Why these matters

A country borrowing at 3% has more room to invest, refinance, and absorb shocks.

A country borrowing at 10% or more has less room for error. Interest payments rise quickly. Budgets tighten. Private credit is expensive. Infrastructure plans slow down. Social spending becomes harder to protect.

For Africa, the issue is not only how much is borrowed. It is whether borrowed money creates enough economic value to justify its cost.

Africa’s Debt Paradox

Africa’s debt paradox is simple: the continent contributes a small share of global debt but pays some of the highest borrowing costs.

In the report’s executive summary, LEAF Africa observes that Africa’s share of global debt stood at about $1.8 trillion, or 1.8% of global debt, while borrowing costs average 8% to 15%, compared with 2% to 3% in advanced economies.

This disparity is not only a financial issue. It is a development issue.

When debt is expensive, governments spend more on servicing loans and less on productive investment. That affects infrastructure, education, healthcare, industrial policy, climate resilience, and support for small businesses.

For entrepreneurs, high sovereign borrowing costs can feed into higher lending rates. For investors, they increased risk premiums. For policymakers, they reduce the flexibility needed to respond to shocks.

Data Interpretation: What the Numbers Really Mean

The headline number, $102 trillion, is important. But the deeper insight is about who can afford debt and who cannot.

Debt sustainability is not determined by debt size alone. It depends on:

- Interest rates

- Currency structure

- Export earnings

- Tax revenue capacity

- Investor confidence

- Debt maturity profile

- Whether borrowed funds are invested productively

This is why two countries can have similar debt levels but very different debt outcomes.

A country with strong tax revenues, deep capital markets, and low borrowing costs can carry higher debt more safely. A country with weak revenue mobilization, high FX exposure, and expensive borrowing can face debt distress at lower debt levels.

The real lesson for Africa

Africa’s debt challenge should not be reduced to “too much debt.”

The better framing is:

Africa needs cheaper, smarter, and more productive borrowing.

That means borrowing funds to grow-enhancing assets, supports private-sector activity, and improves future repayment capacity.

Economic and Investment Implications

For African economies

High borrowing costs reduce fiscal space.

When more public revenue goes into interest payments, governments have less capacity to fund roads, power, schools, health systems, industrial zones, and digital infrastructure.

This can slow growth and deepen dependency on future borrowing.

For investors

Africa’s high borrowing costs create both risk and signal.

They signal macroeconomic vulnerability, but they also highlight where reforms can unlock value. Countries that improve fiscal credibility, stabilize currencies, deepen domestic capital markets, and strengthen institutions can reduce the risk of premiums over time.

For bond investors, this creates a need for country-level differentiation. Africa should not be treated as one risk category.

For entrepreneurs

Sovereign borrowing costs affect private capital.

When governments borrow heavily at high rates, local banks often prefer lending to the state rather than to businesses. This can crowd out private sector credit and make loans more expensive for SMEs, startups, and manufacturers.

For entrepreneurs, the cost of national debt can become the cost of doing business.

Strategic Insight: What This Means for Decision-Makers

For Investors

Investors should look beyond headline debt numbers.

The key questions should be:

- What is the country’s borrowing cost?

- Is the debt local currency or foreign currency?

- How strong is revenue collection?

- Are borrowed funds supporting productive sectors?

- Is the government improving fiscal transparency?

The opportunity lies in identifying countries where the risk premium is high, but reform momentum is credible.

For Policymakers

Policymakers need to focus on debt quality and sustainability, not just debt quantity.

The priority should be to reduce borrowing costs through stronger fiscal management, transparent debt reporting, improved tax mobilisation, domestic capital market development, and better project selection.

Borrowing should be allocated to economic assets that increase productivity and future revenue.

For Entrepreneurs

Entrepreneurs should understand debt as part of the business environment.

High public debt costs can influence exchange rates, inflation, bank lending rates, investor appetite, and public spending. Businesses operating in high-debt economies need stronger pricing strategies, currency risk planning, and diversified funding sources.

The Policy Direction: Borrow Better, Not Just Less

Avoiding debt altogether is not realistic for most economies.

The real policy question is how countries borrow, at what cost, in what currency, and for what purpose.

For Africa, a better debt strategy should include:

- More concessional financing where available

- Stronger domestic revenue mobilization

- Local-currency capital market development

- Transparent debt reporting

- Better public investment management

- Productive use of borrowed funds

- Reduced reliance on expensive commercial borrowing

The goal is not a debt-free Africa. The goal is a continent where debt supports transformation rather than constraining it.

Conclusion: Africa’s Debt Problem Is a Pricing Problem

The world is not moving away from debt. It is moving deeper into it.

However, section 1 of LEAF Africa’s Debt Story report shows that the burden of debt is unevenly distributed. The United States, China, and Japan hold the largest shares of global debt, but Africa faces a much higher borrowing cost despite holding a far smaller portion of the total.

That is the real story.

Africa’s debt challenge is not simply about the amount owed. It is about the price of capital, the structure of borrowing, and the value created from every dollar borrowed.

For decision-makers, the message is clear: the next phase of Africa’s debt conversation must move from fear of debt to discipline around debt. Borrowing can build economies, but only when it is affordable, transparent, and productive.

Go deeper with LEAF Africa

Africa’s debt story is not just about how much the continent owes. It is about the cost of borrowing, the structure of debt, and the choices that shape economic resilience.

Download LEAF Africa’s full Africa’s Debt Story report to explore the data, charts, risks, and opportunities behind Africa’s debt position.

Subscribe to LEAF Africa for clear, data-driven insights on African economies, markets, policy, and investment opportunities.

US-Iran Peace Deal: Africa’s Economic Test

The U.S.-Iran peace framework matters for Africa not because it resolves the continent’s structural vulnerabilities, but because it temporarily reprices several global risks to which African economies are…

Continue reading

Share a market signal, question, or useful perspective. You can respond to the article as a whole, or use the "Discuss this section" buttons beside key points to add context.

The discussion space is open. Add a clear observation, a question worth exploring, or a field signal that could help other readers think more sharply.