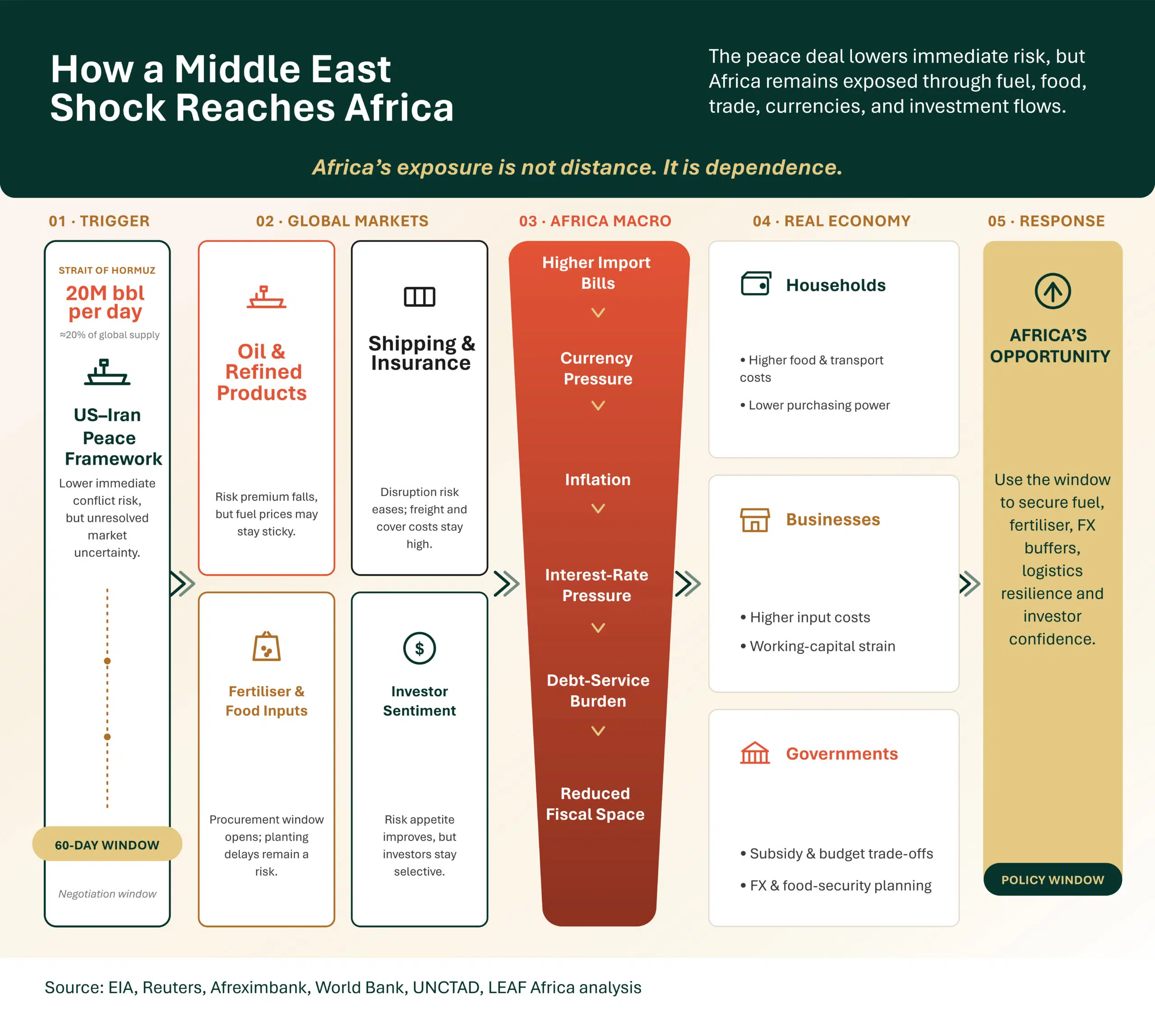

The U.S.-Iran peace framework matters for Africa not because it resolves the continent’s structural vulnerabilities, but because it temporarily reprices several global risks to which African economies are unusually exposed. The reported agreement has reduced the immediate probability of a severe disruption around the Strait of Hormuz and has contributed to a softer oil-risk premium in global markets. Yet the economic implication for Africa is not simple relief. It is a narrow policy window in which governments, firms, and investors can reduce exposure before the next round of commodities, shipping, or currency stress.

The reason is structural. Africa’s exposure to Middle East instability operates less through direct battlefield geography than through prices, balance-of-payments channels, food systems, and financial-market sentiment. Energy import bills feed into transport costs; transport costs influence food prices; food prices shape inflation expectations; inflation affects interest rates, currencies, and debt-service burdens; and these macroeconomic pressures then reach firms and households. In that sense, the peace framework is not only a diplomatic event. It is also a test of whether African economies can convert temporary external relief into greater domestic resilience.

The scale of the underlying chokepoint risk is substantial. In 2024, about 20 million barrels per day of crude oil, condensate and petroleum products moved through the Strait of Hormuz, equivalent to roughly 20% of global petroleum liquids consumption (EIA 2025a). The route is also central to gas markets: about 20% of global liquefied natural gas trade transited Hormuz in 2024, with Qatar alone exporting about 9.3 billion cubic feet per day through the corridor (EIA 2025b). These figures explain why even a partial disruption can move prices far beyond the Gulf. Africa’s vulnerability, therefore, lies not in being the largest direct buyer of Gulf energy but in having limited buffers against the second-round effects of global energy, fertilizer, and freight shocks.

What Has Actually Changed?

The immediate change is that markets now price a lower probability of acute escalation than they did during the peak of the conflict. Reuters reports that the draft U.S.-Iran arrangement included oil-sanctions waivers and reopening of the Strait of Hormuz as part of a 60-day process toward a broader settlement (Reuters 2026a). Following signs of easing supply risks, oil prices declined sharply, with Reuters reporting that Brent Crude fell by more than 3% after talks signaled lower supply-risk concerns and later traded near a four-month low as expectations of smoother Hormuz flows improved (Reuters 2026b; Reuters 2026c). For African economies, this matters because oil prices remain a key external driver of fuel, transport, and food costs.

However, the framework remains fragile and should not be read as full normalization. Iranian state media reported that ships must still request Iran's permission through a newly established Persian Gulf Strait Authority before passing through the Strait of Hormuz. The operative question is not whether vessels can move through the corridor today; it is whether shipping firms, insurers, traders, and lenders believe that passage will remain safe, legally predictable, and affordable over the coming months. The Red Sea crisis demonstrated that maritime disruption could persist even when formal trade routes remain open: UNCTAD documented how attacks and rerouting through the Red Sea and Suez Canal created wider trade-cost and timing effects beyond the immediate conflict area (UNCTAD 2024a). African nations should therefore treat the reported agreement as a short-term reduction in tail risk, not as a permanent solution to chokepoint exposure.

Two layers of impact follow. The first is short-term market relief: a lower oil-risk premium, improved tanker movement, reduced panic in fuel markets, and better planning conditions for importers. The second is medium-term uncertainty: unresolved enforcement issues, possible re-escalation, elevated freight and insurance premiums, and delayed adjustment in fertilizer and refined-product markets. For Africa, the second layer is the more consequential one because domestic pass-through is often slow, uneven, and amplified by exchange-rate weakness.

Why Africa Is Exposed Even When the Conflict Is Elsewhere

Africa’s exposure is rooted in dependence on imported energy, food, fertilizer, refined products, pharmaceuticals, machinery and capital goods, combined with thinner fiscal and external buffers than those of advanced economies. The IMF’s 2026 Regional Economic Outlook for Sub-Saharan Africa emphasizes that many economies entered the period with elevated debt-service pressures and a continuing need to preserve external sustainability and reserve buffers (IMF 2026). This macroeconomic structure makes a global price shock more damaging in Africa than in economies with reserve currencies, deeper fiscal space, or larger strategic inventories.

Food and agricultural-input dependence intensify this vulnerability. Afreximbank estimates that African countries collectively import roughly US$50 billion worth of food annually, leaving the continent exposed to global price volatility and supply disruption (Afreximbank 2024). Fertilizer dependence is also acute: a World Bank analysis notes that approximately 90% of fertilizer consumed in Sub-Saharan Africa is imported, mostly from outside the continent (World Bank 2022). When global fertilizer flows tighten, African farmers face not only higher input prices but also risks to yields, planting decisions and future food inflation.

This is why the African transmission channel is best understood as a chain reaction rather than a single commodity shock. A disruption in oil markets raises fuel and transport costs. Higher transport costs raise the cost of moving food, inputs, and manufactured goods. Rising food prices increase headline inflation and social pressure. Inflation and foreign exchange demand weaken currencies and compel monetary policy tightening. The result is a macroeconomic event that begins in global energy markets but ends in African household budgets, business working capital, and public-sector financing needs.

Energy Markets: Importer Relief, Exporter Ambivalence

Energy is the most immediate transmission channel. If the reported agreement holds, lower perceived supply risk should reduce upward pressure on crude and refined-product prices. This is particularly important for African economies that rely heavily on imported fuel and refined petroleum products. Lower prices can reduce import bills, ease demand for foreign exchange, moderate transport costs, and lower the fiscal pressure associated with fuel subsidies or regulated pump prices. These effects do not require Africa to be the principal buyer of Gulf oil; they flow through the global price of crude, refined products, and shipping.

The relief, however, will not be instantaneous. Pump prices in many African countries reflect not only crude prices but also exchange rates, import timing, taxes, levies, storage costs, port charges, inland logistics, regulated pricing mechanisms, and the price at which existing inventories were purchased. Consequently, a decline in international crude prices can reach households and firms with a lag. The World Bank’s April 2026 Commodity Markets Outlook projected a 24% increase in energy prices in 2026 under the Middle East shock, illustrating how quickly geopolitical risk can reverse the disinflation gains that many economies had been expecting (World Bank 2026a). Even if prices subsequently ease, the pass-through to consumers may remain sticky.

For hydrocarbon exporters, the balance is more complex. Lower geopolitical risk reduces volatility and can support macroeconomic planning, but it can also reduce the windfall revenue that higher oil prices temporarily provide. The distinction between crude exporters and refined-product importers is important: an oil-producing country may still face domestic fuel inflation if refining constraints, exchange-rate pressures, and distribution costs keep local fuel markets expensive. The policy implication is therefore not that peace is uniformly positive or negative for all African countries. It is that the balance of gains depends on each country’s net energy position, exchange-rate regime, fuel-pricing framework, and fiscal dependence on hydrocarbon revenues.

Food and Fertilizer: The Delayed Transmission Channel

The food-security channel is slower than the fuel-price channel, but it may be more socially consequential. Fertilizer is not simply another import category; it is a productivity input that influences crop yields, farm income and food affordability. The World Bank’s June 2026 Food Security Update reports that disruptions to oil, gas and fertilizer flows through the Strait of Hormuz drove a 46% month-on-month rise in urea prices and an 8% increase in agricultural price indices; the same update projects that fertilizer prices will rise by 31% on average in 2026, reaching their least affordable levels since 2022 (World Bank 2026b). These figures show why African policymakers cannot judge the agreement only through crude-oil prices.

The risk is temporal. A political agreement can lower immediate energy-market stress while leaving fertilizer procurement and planting decisions exposed. If fertilizer shipments are delayed or remain expensive during procurement windows, farmers may reduce application rates. Lower applications can depress yields; lower yields can push food prices higher; and higher food prices can intensify inflation, wage pressure, and poverty risks. In low-income households, food absorbs a large share of expenditure, making food inflation especially damaging even when the initial shock occurs far from the continent.

The reported 60-day window should therefore be treated as a procurement and risk-management opportunity. Governments, agribusinesses, and input distributors can utilize the period to secure fertilizer supply, diversify sources, coordinate regional procurement, strengthen port clearance, and reduce financing bottlenecks for importers and farmers. This response is more credible than waiting for markets to normalize. Given Sub-Saharan Africa’s high fertilizer-import dependence, the strategic question is not only whether fertilizer prices fall, but whether inputs arrive on time and at prices farmers can afford (World Bank 2022; World Bank 2026b).

Trade and Logistics: A Breather, not a Full Reset

The peace framework also gives African trade a logistics breather. Functioning Gulf routes reduce the probability of wider disruptions to energy, fertilizer, petrochemicals, aviation links, construction inputs, and consumer goods. Yet maritime evidence from recent years suggests that trade-route stability is increasingly fragile. Global maritime trade reached 12.3 billion tons in 2023 and was projected by UNCTAD to grow by about 2% in 2024, but UNCTAD also warned that geopolitical conflict, climate disruption and volatile freight costs were weighing on a durable recovery (UNCTAD 2024b). Africa’s exposure to these pressures is magnified by port bottlenecks, high logistics costs, and dependence on imported intermediate goods.

Chokepoint risk is not limited to Hormuz. The Red Sea, Suez Canal, Bab el-Mandeb, and Cape of Good Hope have all become part of the continent’s trade-resilience conversation. UNCTAD’s assessment of the Red Sea disruption reported major rerouting pressures and a reported 40% decline in Suez Canal revenues, underscoring how quickly maritime instability affects trade costs, port schedules and public revenues in regions connected to global shipping corridors (UNCTAD 2024a). For Africa, the implication is clear: even when one corridor stabilizes, the vulnerability created by concentrated routes and weak logistics redundancy remains.

This creates two policy opportunities. First, African ports that receive rerouted or repositioned traffic should convert temporary attention into measurable improvements in clearance, storage, hinterland connectivity, and shipping reliability. Second, the African Continental Free Trade Area should be treated as part of a resilience strategy, not only as a market-integration project. Intra-African trade will not replace global supply chains quickly, but deeper regional sourcing can reduce exposure to external chokepoints over time. The peace framework reduces pressure; it does not remove the structural case for logistics reform.

Investment Flows: Lower Risk Premiums, Higher Country Differentiation

Geopolitical conflict typically raises uncertainty, energy-price volatility, inflation expectations, and risk premia for emerging and frontier markets. A credible de-escalation can therefore support lower spreads, stronger investor sentiment, and renewed interest in project finance. The World Bank’s June 2026 Global Economic Prospects warns, however, that global growth is expected to slow to 2.5% in 2026, the weakest pace outside outright recession in nearly two decades, with commodity disruptions and policy uncertainty remaining key downside risks (World Bank 2026c). That environment makes capital more selective rather than universally abundant.

Africa will therefore not be repriced as a single asset class. Countries with stronger fiscal credibility, more transparent exchange-rate policy, lower fuel-import vulnerability, credible inflation management, resilient logistics systems, and predictable investment rules are better positioned to benefit from a decline in geopolitical risk premium. Countries with high debt-service obligations, limited reserves or large fuel and food import bills may experience only partial relief because investors will continue to assess domestic fundamentals alongside external de-escalation. The IMF’s emphasis on reserve preservation and fiscal consolidation in Sub-Saharan Africa reinforces this point (IMF 2026).

Africa’s Geopolitical Positioning: From Price-Taker to Strategic Actor

The peace agreement also has geopolitical implications for Africa.

For years, Africa has often been treated as a receiver of external shocks: oil shocks, food shocks, debt shocks, and currency shocks. The US-Iran conflict has shown again how quickly global power competition can reshape African economic conditions.

But Africa is not without leverage.

The continent sits at the center of several strategic interests: critical minerals, energy transition inputs, food systems, young consumer markets, maritime routes, and diplomatic votes in multilateral institutions. Gulf countries, China, Europe, the United States, India, and Turkey all have expanding interests in African markets.

The peace agreement creates room for African states to reposition.

A stronger African response would focus on three priorities:

1. Energy diplomacy

Africa should negotiate energy security arrangements that go beyond emergency imports. This includes refining capacity, gas infrastructure, storage, renewable energy deployment, and regional power pools.

2. Food-security diplomacy

Fertilizer access should be treated as a strategic security issue. Africa needs better procurement coordination, regional fertilizer production, port efficiency, and financing tools for farmers.

3. Maritime and trade diplomacy

African coastal and island states should play a stronger role in conversations about shipping security, port resilience, and trade-route diversification.

The peace agreement is therefore not only a market event. It is a reminder that African countries need a clearer external economic strategy in a more fragmented world.

Risks and Opportunities for Africa After the Peace Deal

Key risks

- False relief

Oil prices may fall before supply chains fully normalize. Policymakers may relax too early.

- Sticky prices

Fuel, food, and transport costs may remain high even after crude prices ease.

- Fertilizer lag

Input prices can remain elevated long enough to affect planting, yields, and food prices.

- Fiscal slippage

Governments may reintroduce broad subsidies or spend savings instead of rebuilding buffers.

- Renewed escalation

The 60-day framework is still a negotiation window. A breakdown could quickly restore the risk premium.

Key opportunities

- Lower import pressure

Fuel-importing countries can rebuild reserves and reduce pressure on exchange rates.

- Better procurement timing

Governments and agribusinesses can secure fertilizer and energy supplies before prices harden again.

- Investor re-entry

Reduced geopolitical risk can support renewed interest in African sovereign bonds, infrastructure, and trade finance.

- Logistics repositioning

African ports and corridors can use the disruption to strengthen their role in alternative trade networks.

- Policy credibility gains

Countries that respond with discipline, not panic, can attract capital faster.

The policy message is direct: external peace can create breathing space, but domestic credibility determines whether that breathing space becomes capital inflow, lower borrowing costs, or stronger investment pipelines. For investors, the opportunity is to distinguish between economies where the shock exposed structural fragility and those where credible reform momentum can convert lower external risk into improved macroeconomic performance. For African policymakers, the lesson is sharper still: the best response to a temporary geopolitical reprieve is not complacency, but faster preparation for the next shock.

Go deeper with LEAF Africa

The US-Iran peace deal is not just a foreign policy event. It is a signal for African energy security, food systems, trade routes, inflation, and investment strategy.

Download LEAF Africa’s latest reports for clear, data-driven insight into Africa’s macroeconomic risks, market opportunities, and policy direction.

Subscribe to LEAF Africa for sharp analysis on African economies, capital markets, trade, and investment flows.

Africa’s $1.9 Trillion Debt Question

Africa’s public debt expanded from $510 billion in 2008 to $1.83 trillion in 2024, a 253% increase in 16 years. But the deeper story is not just how…

Continue reading

Share a market signal, question, or useful perspective. You can respond to the article as a whole, or use the "Discuss this section" buttons beside key points to add context.

The discussion space is open. Add a clear observation, a question worth exploring, or a field signal that could help other readers think more sharply.